What is an appraisal?

Once a home buyer goes under contract to purchase a property, their lender will hire an appraiser for the property. This is to assure that the amount the bank is lending to the borrower for the property being purchased, does not exceed what the property is worth. It makes complete sense. Who would want to lend money on an overvalued property? So picture this…

You put in an offer to buy your dream home! This is the most exciting time of your life! You have been picking out furniture online so you can have your housewarming party ASAP. You have asked your friends for references for the back deck you are dying to put on just in time for grilling season. You have already picked out the paint colors for the new babies room (Lemon Chiffon) and the last thing on your mind was a low appraisal…

OR

You are selling your house after struggling for a while. A couple of years ago your house was underwater, but now that values have crept back up you can finally sell. This 2 bedroom 1 bath starter home is just too small with 2 kids and your parents visiting twice a month, but your next big move is in sight. You found the perfect neighborhood, with great schools, a short commute to work and a huge backyard for the kids to run and play. The last thing on your mind was a low appraisal…

The lender calls and says I’m sorry, but you had a low appraisal on the property.

Total devastation because what do you do now?

First off, don’t panic. Low appraisals happen everyday, all over the country. In your purchase contract, you should have a mortgage contingency. Mortgage contingency makes the purchase of the property dependent on the buyer securing financing for a specific percentage of the total purchase price. So if John Doe is putting down 5% on a $100,000 property, he is taking out a loan of 95% of the value of that property or $95,000. If he was putting down 10% on the property his loan would be 90% of the value of the property or $90,000 etc. The buyer will write into the contract how much money they are borrowing against the purchase price known as “loan to value.” The financing is contingent upon the property appraising out at the purchase price or above.

Let’s walk through that in English:

Jane buys a $100,000 property and is putting down 10%.

The property appraises out at $93,000, but the purchase contract is for $100,000.

The bank will only loan Jane 90%(since they are putting down 10% of their own money) of the appraisal of $93,000 which is $83,750.

The mortgage contingency made the purchase contract contingent of John getting a mortgage of 90% of his purchase price. Because of the low appraisal, John cannot receive financing for 90% of $100,000, but he can obtain financing for 90% of $93,000 (the appraisal amount).

If Jane wants to buy this house they have 2 options because of the low appraisal.

1. They can come up with the extra $6,200 in addition to the 10% down payment.

OR

2. They can go back to the seller and see if the seller will agree to a $93,000 sales price because of the low appraisal.

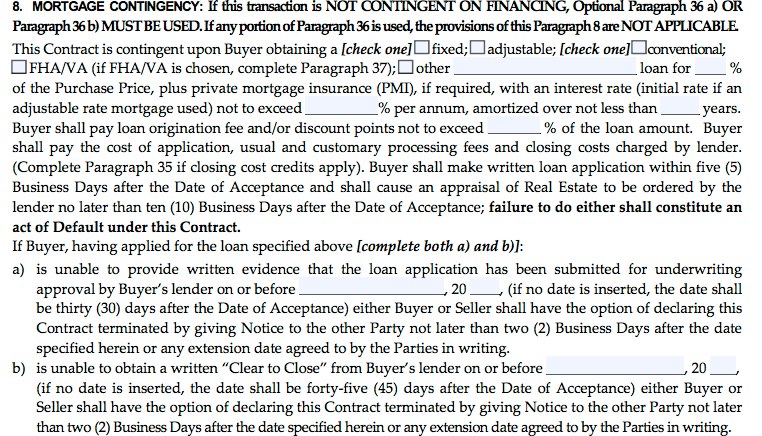

This is what the mortgage contingency looks like in the standard 6.0 contract that is typically used in the Chicago real estate market.

Here are a couple tips to make sure a low appraisal does not happen to you. The best thing you can do is be proactive so you don’t end up dealing with the hassle of a low appraisal.

1. Don’t overpay for a house. Look at recent sales prices in your area and figure what what homes are really selling for, not just a listing price.

2. Do your homework. Make sure you have a good mortgage contingency in your contract and a fall back plan.

3. Do not buy without an experienced real estate agent(who will take care of #1 and #2)